Operating environment

Operating environment

Mandatum is a financial services provider that operates both in the asset and the wealth management and insurance markets. Its wide range of services includes asset and wealth management, pension plans, compensation and rewards, as well as personal risk insurance. The key markets are expected to grow over the next years.

Mandatum has its roots in Finland, where it offers the full variety of its services. In Finland, the company serves some 250,000 retail clients and around 20,000 companies. The asset management business is international and has expanded especially to Sweden, but also to other Nordic countries and into Central Europe.

MARKET GROWTH SUPPORTS MANDATUM’S GROWTH OBJECTIVES

The key markets for Mandatum in asset management, private wealth management, as well as corporate pension and personal risk insurance have developed favourably in recent years, and their growth is expected to remain strong in the coming years.

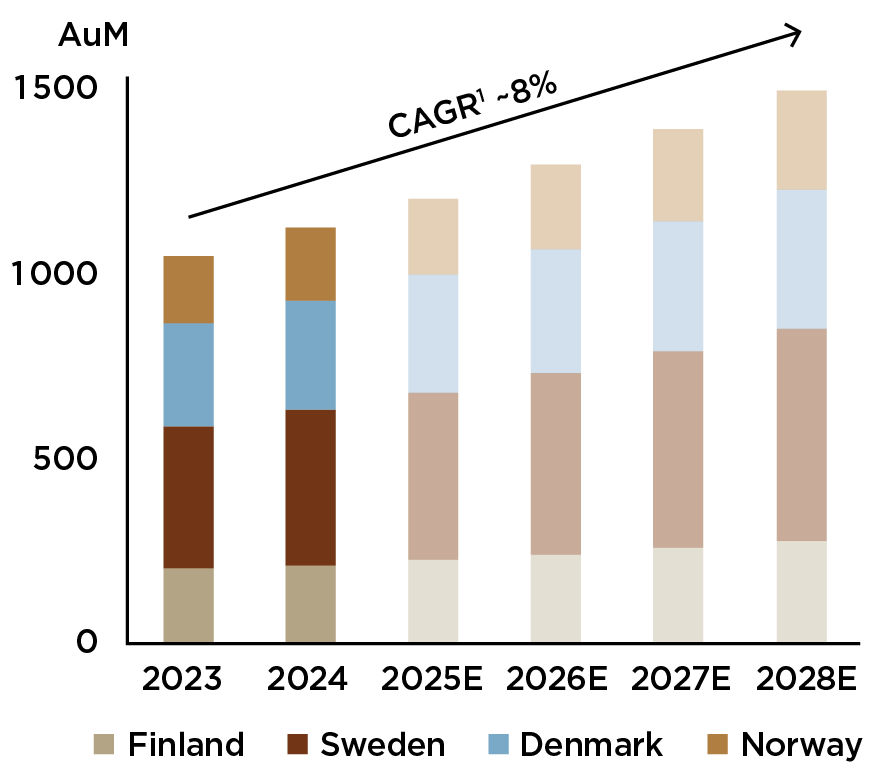

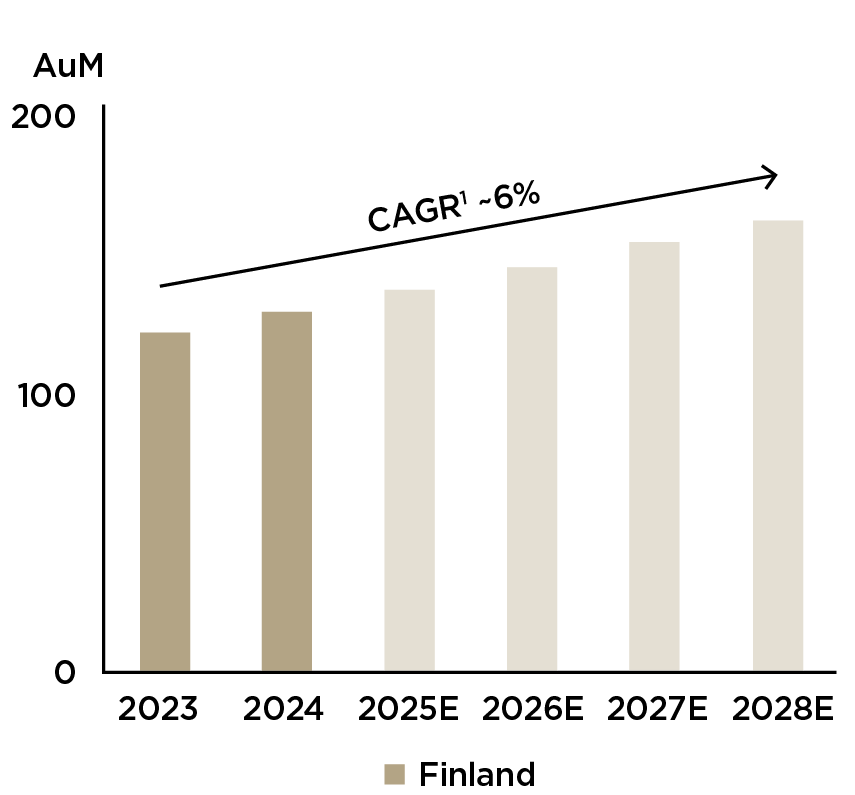

The value of the Nordic asset management market already exceeds EUR 1,000 billion and it is expected to grow at a compound annual growth rate (CAGR) of around 8 per cent in the coming years. In Finland, the private wealth management market CAGR is expected to be around 6 per cent. Factors influencing this development include the growth of Nordic economies, creation of new wealth by the corporate sector, and the transfer of accumulated wealth to the next generations.

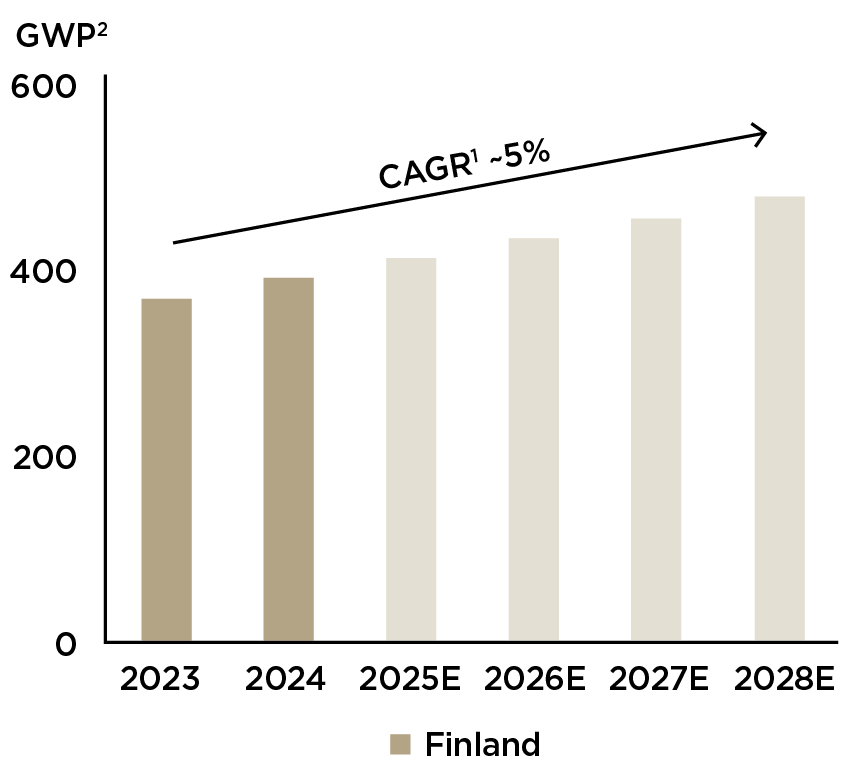

In the corporate unit-linked pension insurance and corporate personal risk insurance market, the CAGR for premiums written is expected to be around 5 per cent in the coming years. Factors influencing the pension insurance market growth include the ageing of Finland’s population and the weakening of social security. As a result, the need for individuals to supplement their statutory pensions with voluntary pension savings has grown. Companies have also assumed a more prominent role in supplementing employees’ insurance cover, and the popularity of insurance benefits offered as employee benefits has increased in Finland in recent years. The CAGR for corporate personal risk insurance market (including life insurance and cover for serious illness and disability) is expected to be around 7 per cent in the coming years.

Asset management market in the Nordics³ (AuM EUR billion)

Private wealth management market in Finland³ (AuM EUR billion)

Corporate unit-linked pension and corporate personal insurance market in Finland³ (Gross written premium EUR million)

1) Compound Annual Growth Rate (CAGR)

2) Gross written premium

3) Based on third-party market study and company estimates